A Guide to Merchant Risk Classification

Merchants may be considered high-risk for a myriad of reasons. What many people do not realize is that all card not present (CNP) transactions are considered to be higher risk by the banks and thus incur higher processing fees than card present (CP) transactions.

Today, CNP transactions are seen as increasingly risky because EMV adoption has moved cyber criminals to ecommerce. This means merchants who accept CNP transactions are at increased risk of fraud and charge-backs unless they have the right risk management tools and a processing partner who understand the unique challenges facing CNP merchants.

Businesses May Be Classified High-Risk Due To:

- • Merchant Category Code (MCC)

- • Reputational Risk for the Bank

- • Poor Credit Score

- • High Chargebacks

- • High Refunds

- • High-Ticket

- • Trial Offers

- • Subscription and Continuity

Guidelines Bank’s Use to Assess Risk:

Ultimately, a bank’s underwriting guidelines will determine whether they consider a merchant high risk. In addition to the credit worthiness and processing history, the underwriters will determine the risk of chargebacks and fraud associated with that industry. For example, travel and tour operators are considered high-risk because weather and outside factors create cancellations and charge-backs. Adult entertainment, gambling, firearms, knives, tobacco are prohibited by many banks for reputational risk and/or high charge-backs.

If a merchant is launching a new business without processing history the credit score and merchant classification code will be important considerations. While each processor calculates risk differently, charge-backs and reputational risk are key factors in their final decision. A merchant with a history of excessive chargebacks will need to explain why, and most importantly, have a plan in place to avoid high chargebacks in the future. This is why experience and relationships in high-risk matter a great deal.

DigiPay Solutions and High-Risk Merchants

At DigiPay relationships matter. We work collaboratively with high-risk merchants and partner banks and we have earned their trust by operating with integrity, intelligence, and transparency. Our banking partners appreciate that we have in-house underwriters and risk managers who mirror underwrite and manage risk using their guidelines. For high-risk merchants this means faster approvals and a stronger banking relationship because your account is set-up properly, and risk flags are quickly identified and addressed to avoid closure.

Our goal is for every business to succeed and thrive because the more transactions a high-risk merchant processes the more we both profit. This is why we use technology and human intelligence to ensure every high-risk merchant is compliant with all governing regulatory bodies and that they are educated about ever evolving changes.

In addition to enterprise level high-risk merchants we work with new ventures and merchants who have little or no credit history. If a merchant has had an account terminated or they have a history of high-chargebacks or refunds, we have the knowledge and experience to create a plan to rehab the account.

All client information is confidential and stored securely and in compliance with PCI standards. Our application process is simple and we work closely with merchants to make sure all underwriting packages are complete and the business is presented in the best possible light.

High-Risk Q & A

How Do Processors Compare High-Risk Merchants to Low-Risk?

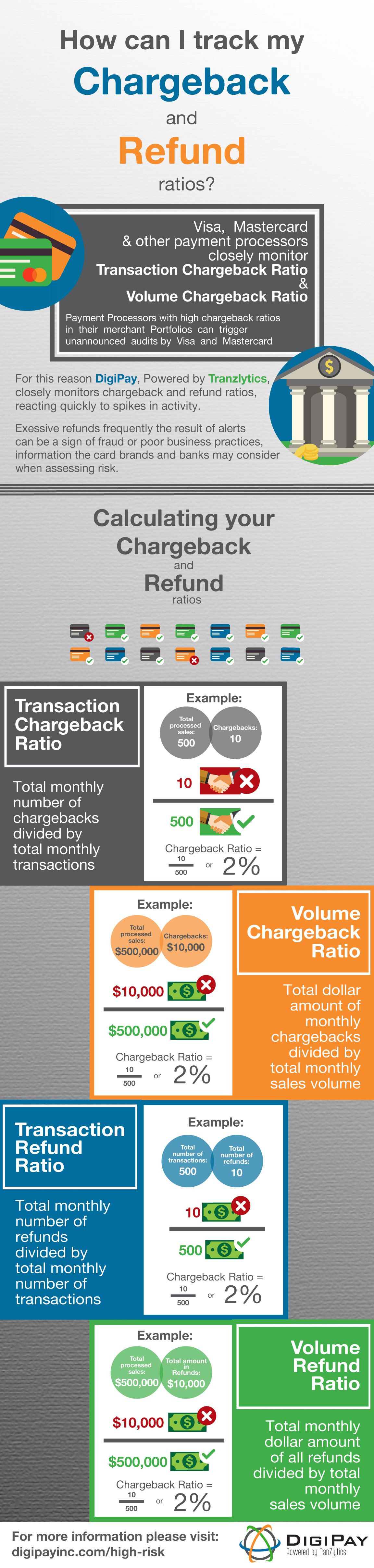

Chargeback thresholds and merchant category code will largely determine whether a merchant is classified as high-risk or low-risk. With respect to chargeback thresholds, the acquiring banks and processors expect chargebacks to be below 1% of total transactions. For information on how to calculate your chargeback rate check out the infographic below.

How to Calculate Your Chargeback Ratio

What if Chargebacks Exceed 1%?

When chargebacks exceed 1% the merchant account is flagged by risk and may be required to enroll in a chargeback monitoring program. These programs work very differently for merchants that are classified as high-risk. While low-risk merchants will be given time to address the issues creating chargebacks, they are typically not assessed high fees. High-risk merchants may be immediately subject to extremely high-fees and escalating penalties for unabated high-chargebacks. If chargeback trends show continued escalation the merchant account may be closed or terminated.

What is the Difference Between a Closed Merchant Account and a Terminated Merchant Account?

The difference between a closed merchant account and a terminated merchant file (TMF) aka the Match List, which stands for Merchant Alert to Control High-Risk is critical because a TMF not only stops you from processing credit cards in the present, it prevents you from obtaining a merchant account in the future under any other business names for five years. This is the length of time you will remain in the database according to MasterCard. This link provides important information from MasterCard about the MATCH list and Online Learning Materials.

When a merchant account is closed for high-chargebacks it does not necessarily mean it was placed on the MATCH list. Unfortunately, many merchants are not aware they are on the MATCH list until they try to acquire a new merchant account. The reason merchants are added to the MATCH database is fairly extensive, but the reason codes are related to:

- • Excessive chargebacks

- • Participating in fraudulent activities

- • Collusion

- • Violation of standards and compliance regulations

- • Identity theft

- • Money laundering

If you discover you are on the MATCH list contact the bank that added you to the list and call them to find out what you can do to be removed from the list. If the reason is related to fraud your only recourse may be to engage legal counsel. If it is excessive chargebacks the banks may be more forgiving and allow time for corrective action and restitution if chargebacks exceed reserves.

How Does High Risk Classification Affect Credit Card Processing?

Even if a business is considered high risk they can still can accept credit payments. However, these businesses will pay higher processing rates and the bank may require an upfront or rolling reserve on a business’ credit card processing.

Can High-Risk be Reclassified?

Depending on why a merchant is classified as high-risk some banks will reclassify a business. If the merchant category code (MCC) is the reason for high-risk classification then it is not possible to reclassify. However, if the MCC is not high-risk and the merchant has a positive credit card processing history over six months with a small number of chargebacks and refunds reclassification may be possible.

How Do I Apply for A DigiPay Merchant Account?

We make it simple. Fill out our online application and one of our high-risk specialists will reach out to discuss which banking partner offers the best rates and terms and conditions based on your merchant category code and processing history.

About The Author: Sandy Travers

Payment technology executive Sandra Travers is Co-Founder & Co-CEO of DigiPay Solutions, Inc.. Her years of experience in early-stage technology ventures brings a unique perspective to payments. Sandra manages operations and risk in addition to new product development.

More posts by Sandy Travers